Cookbook

All the examples presented below can be found in examples. For the details of each function or class, refer to the API documentation (pyanomaly).

First, import the packages as follows:

import matplotlib.pyplot as plt

from pyanomaly.globals import *

from pyanomaly.fileio import read_from_file

from pyanomaly.characteristics import FUNDA, FUNDQ, CRSPM, CRSPD, Merge

from pyanomaly.jkp import make_factor_portfolios

from pyanomaly.tcost import TransactionCost, TimeVaryingCost

from pyanomaly.analytics import *

from pyanomaly.wrdsdata import WRDS

Example 1

Firm characteristics generation replicating JKP.

This example shows the full process of i) data download, ii) factor creation, and iii) characteristics creation. This example replicates the JKP’s SAS code as closely as possible.

In this example,

funda is merged with fundq to create quarterly updated annual accounting data.

The latest market equity (me) is used when creating firm characteristics.

Generate firm characteristics that appear in the JKP’s paper.

- Note:

Some firm characteristics’ definitions are different from those of JKP’s. To follow JKP’s definitions, set

config.REPLICATE_JKP = True. This will make the program use JKP’s definitions when possible.config.REPLICATE_JKPis only for verification purpose and will be deprecated.

Initialization

Set the log file path and initialize time check (can be skipped).

# Set log file path. Without this, the log will be printed in stdout.

set_log_path('./log/example1.log')

# initialize time check.

elapsed_time('Start of Example 1.')

Data download

Download data frm WRDS.

wrds = WRDS(wrds_username) # Use your WRDS user id.

# Download all necessary data.

wrds.download_all(run_in_executer=False) # run_in_executer=True will download faster but consumes more memory.

# Create crspm(d) from m(d)sf and m(d)seall and add gvkey to them.

wrds.preprocess_crsp()

Factor generation

Generate FF3 and HXZ4 factors. These are used in some firm characteristics, such as the residual momentum.

make_factor_portfolios(monthly=True) # Monthly factors

make_factor_portfolios(monthly=False) # Daily factors

Characteristic generation

# Generate characteristics in 'jkp' column in mapping.xlsx.

alias = 'jkp'

# Start date. Set to None to create characteristics from as early as possible.

sdate = '1950-01-01'

###################################

# CRSPM

###################################

# Generate firm characteristics from crspm.

crspm = CRSPM(alias=alias)

# Load crspm.

crspm.load_data(sdate)

# Filter data on shrcd, ...

crspm.filter_data()

# Fill missing months by populating the data.

# There are only few missing data and the results aren't affected much by this.

crspm.populate(freq=MONTHLY, method=None)

# Some preprocessing, e.g., creating frequently used variables.

crspm.update_variables()

# Merge crspm with the factors created earlier.

crspm.merge_with_factors()

# Display what characteristics will be generated. Just for information.

crspm.show_available_functions()

# Create characteristics.

crspm.create_chars()

# Postprocessing: delete temporary variables, etc.

crspm.postprocess()

# Saves the results. You can give a file name if you wish. Otherwise, the file name will be the lower-case class

# name, i.e., crspm. The file can later be loaded using the method, crspm.load().

crspm.save()

###################################

# CRSPD

###################################

# Generate firm characteristics from crspd.

crspd = CRSPD(alias=alias)

# Load crspd.

crspd.load_data(sdate)

# Filter data on shrcd, ...

crspd.filter_data()

crspd.update_variables()

crspd.merge_with_factors()

crspd.show_available_functions()

crspd.create_chars()

crspd.postprocess()

crspd.save()

###################################

# FUNDQ

###################################

# Generate firm characteristics from fundq.

fundq = FUNDQ(alias=alias)

# Load fundq.

fundq.load_data(sdate)

# fundq has some duplicates (same datedate/gvkey). Drop duplicates.

fundq.remove_duplicates()

# Convert values in another currency (currently only CAD) to USD values.

fundq.convert_currency()

# Populate data to monthly.

fundq.convert_to_monthly()

# Make quarterly variables from ytd variables and use them to fill missing quarterly variables.

fundq.create_qitems_from_yitems()

fundq.update_variables()

fundq.show_available_functions()

fundq.create_chars()

fundq.postprocess()

fundq.save()

###################################

# FUNDA

###################################

# Generate firm characteristics from funda.

funda = FUNDA(alias=alias)

# Load fundq.

funda.load_data(sdate)

funda.convert_currency()

funda.convert_to_monthly()

# Generate quarterly-updated funda data from fundq and merge them with funda.

funda.merge_with_fundq(fundq)

funda.update_variables()

# Add the market equity of crspm to funda.

funda.add_crsp_me(crspm)

funda.show_available_functions()

funda.create_chars()

funda.postprocess()

funda.save()

###################################

# Merge

###################################

# Combine everything together and generate firm characteristics that require data from multiple data sources.

merge = Merge()

# Merge all data together.

merge.preprocess(crspm, crspd, funda, fundq)

merge.show_available_functions()

merge_chars = merge.get_available_chars()

merge.create_chars(merge_chars)

merge.postprocess()

# By default, `Panel.save()` saves all the columns of `Panel.data`.

# If you want to save only the variables you need to save the disc space, you can do, e.g.:

# columns = ['gvkey', 'datadate', 'primary', 'me', 'ret', 'exret', 'rf']

# merge.save(other_columns=columns)

# Then, all firm characteristics plus the columns in `columns` will be saved.

merge.save()

elapsed_time('End of Example 1.')

Example 2

Different ways of generating characteristics.

This example demonstrates

how to generate a few selected firm characteristics without adding a column to mapping.xlsx;

how to set the output file path instead of the default path.

It is assumed that data has been downloaded from WRDS.

Short-term reversal and 12M-momentum will be generated.

alias is set to None, which means function names are used as aliases.

elapsed_time('Start of Example 2.')

alias = None # alias = function names

sdate = None # create characteristics from as early as possible.

# Characteristics to generate: short-term reversal and 12M-momentum.

chars = ['ret_1_0', 'ret_12_1']

# Generate firm characteristics from crspm.

crspm = CRSPM(alias=alias)

crspm.load_data(sdate)

# Filter data on shrcd, ...

crspm.filter_data()

# Let's skip populate() to save time as it doesn't change the result much.

# crspm.populate(freq=MONTHLY, method=None)

# Some preprocessing, e.g., creating frequently used variables.

crspm.update_variables()

# Give a list of characteristics to generate.

crspm.create_chars(chars)

crspm.postprocess()

# Save the output to ./output2/example2.pickle.

# `other_columns=[]` will save only the characterisitcs.

crspm.save('example2', fdir='output2', other_columns=[])

elapsed_time('End of Example 2.')

Example 3

Firm characteristics using year-end ME.

This example demonstrates how to generate funda firm characteristics using year-end ME instead of the latest ME.

All firm characteristics defined in FUNDA are generated.

Only USD-denominated stocks are sampled: currency conversion is unnecessary.

Only funda is used without merging with fundq: merging the two datasets as in Example 1 is also possible.

It is assumed that funda data is available 6 months later.

It is assumed that data has been downloaded from WRDS.

Set variables

alias = None # Generate all characteristics.

sdate = None # create characteristics from as early as possible.

Market equity

# Load crspm as we need ME.

crspm = CRSPM(alias=alias)

crspm.load_data(sdate)

# Preprocessing

crspm.filter_data()

crspm.populate(freq=MONTHLY, method=None)

# 'me' and 'me_company' (firm-level me) are generated here.

crspm.update_variables()

Firm characteristics

funda = FUNDA(alias=alias)

funda.load_data(sdate)

# USD stocks only. This is equivalent to funda.data = funda.data[funda.data['curcd'] == 'USD']

funda.filter(('curcd', '==', 'USD'))

funda.convert_to_monthly(lag=6) # lag=6 means funda is available 6 months later.

funda.update_variables()

# Add year-end market equity to funda.

funda.add_crsp_me(crspm, method='year_end')

# Generate firm characteristics.

funda.show_available_functions()

funda.create_chars()

# Postprocess and save results.

funda.postprocess()

funda.save('funda_eg3')

Example 4

Defining a new characteristic.

This example demonstrates how to define a new class by inheriting CRSPM and add a new characteristic.

A new characteristic, ‘excess_ret_change’, will be added, which is defined as the excess return over the market return divided by the one-year average excess return (I have no idea if this has any predictive power).

It is assumed that data has been downloaded from WRDS.

Defining a new characteristic function

Define a new class by inheriting CRSPM and add a new function c_excess_ret_change() that defines

the new characteristic.

class MyCRSPM(CRSPM):

# Function for the new characteristic.

# Note that function name should be of the form 'c_[characteristic name]'.

def c_excess_ret_change(self):

"""Change of excess return over the market return."""

# Make a short (one-line) docstring for description.

# This is displayed when `show_available_functions()` is called.

cm = self.data

# One-year average excess return

avg_exret = self.rolling(cm.exret - cm.mktrf, 12, 'mean')

# Excess return.

exret = cm.exret - cm.mktrf

# Characteristic

char = exret / avg_exret

return char

New characteristic generation

alias = None # alias = function names

sdate = None # create characteristics from as early as possible.

# Characteristics to generate: the function name is the characteristic name without alias.

chars = ['excess_ret_change']

# Instantiate the class defined above.

crspm = MyCRSPM(alias=alias)

crspm.load_data(sdate)

crspm.filter_data()

crspm.update_variables()

# We need to add factors as we need the market return.

crspm.merge_with_factors()

# Let's see if 'excess_ret_change' has been added.

crspm.show_available_functions()

# Let's create the characteristic!

crspm.create_chars(chars)

crspm.postprocess()

crspm.save('example4')

# Later, you can load the saved file using 'read_from_data()'

data = read_from_file('example4')

print(data['excess_ret_change'])

Example 5

Sorting-based portfolio analysis.

This example demonstrates how to construct quantile portfolios and carry out 1-D or 2-D sorts.

Quintile portfolios will be generated from the 12-month momentum and their mean returns and t-values will be computed.

5x5 2-D sort will be conducted on momentum and size.

Firm-level cross-sectional regression will be conducted.

Factor regressions will be carried out using FF 3-factors.

It is assumed that the firm characteristic has been created and saved to ‘crspm.pickle’.

See also pyanomaly.jkp module for factor and characteristic portfolio creation replicating JKP’s SAS code.

Set variables

char = 'ret_12_1' # 12-month momentum

char_class = char + '_class' # Group column: portfolio-stock mapping

ret_col = 'futret' # Future return column

weight_col = 'me' # Market equity column

split = 5 # Qintile. You can also do split = [0.2, 0.4, 0.6, 0.8].

labels = ['H', 2, 3, 4, 'L', 'H-L'] # Portfolio names: 'H-L' for long short.

Load data

# Read crspm data (not raw data but the output data).

data = read_from_file('crspm')

# If you want to exclude bottom 20% based on NYSE size...

data['nyse_me'] = np.where(data.exchcd == 1, data[weight_col], np.nan) # NYSE me

data = filter(data, weight_col, (0.2, None), by='nyse_me')

# Make the future return. If it's already in the data, this step can be skipped.

data[ret_col] = make_future_return(data['exret']) # Excess return

# Note that the future return at t is the return between t and t+1 and other values are as of t.

# If you want the return at t to be the return between t-1 and t and all other values as of t-1,

# you have to shift forward data as follows.

data = data.groupby(level=-1).shift(1) # Shift data forward.

data = data.dropna(subset=[ret_col]) # Drop nan returns.

1-D sort

# Classify stocks based on char.

data[char_class] = classify(data[char], split, ascending=False)

# Make quantile portfolios.

# qpfs will have index = date/classes and columns = ['futret']

qpfs = one_dim_sort(data, char_class, ret_col, weight_col=weight_col)

# You can add more columns to the portfolios. Here I add `signal` (mean of the characteristic) and

# n_firms (number of firms).

qpfs[['signal', 'n_firms']] = one_dim_sort(data, char_class, char, function=['mean', 'count'])

# If you want to see the average size and price of the portfolios...

qpfs[['size', 'prc']] = one_dim_sort(data, char_class, [weight_col, 'prc'])

# Name the portfolios. Without this, the names are 0, 1, ...

relabel_class(qpfs, labels)

print(f'Quantile portfolios sorted on {char}')

print(qpfs)

# Calculate the time-series mean and t-value of the future return for each portfolio.

# avg and tval have index values equal to the portfolio names.

avg, tval = time_series_average(qpfs[ret_col], cov_type='HAC', cov_kwds={'maxlags': 12})

print(f'\n Mean of portfolio returns sorted on {char}')

print(avg)

print(tval)

# Put them together to make a nice table.

print(pd.concat([avg, tval], axis=1, keys=['mean', 't-val']))

Output:

Quantile portfolios sorted on ret_12_1

futret signal n_firms size prc

date ret_12_1_class

1927-01-31 H -0.010 0.482 69 85.210 73.924

2 0.009 0.151 69 131.678 89.196

3 -0.001 0.013 69 91.500 83.021

4 -0.004 -0.106 69 54.869 54.849

L -0.005 -0.329 69 25.706 34.803

H-L -0.005 0.811 0 59.504 39.120

1927-02-28 H 0.055 0.442 71 97.356 81.886

2 0.040 0.151 70 130.918 89.640

3 0.028 0.048 71 77.347 74.449

4 0.048 -0.074 70 55.549 52.839

L 0.067 -0.299 71 26.083 34.153

H-L -0.012 0.741 0 71.273 47.732

... ... ... ... ...

2020-12-31 H 0.057 1.188 442 27538.688 118.659

2 0.024 0.174 442 23863.618 115.923

3 0.038 -0.042 442 20827.442 867.161

4 0.066 -0.208 442 11994.607 70.635

L 0.070 -0.444 442 6082.012 34.062

H-L -0.013 1.631 0 21456.676 84.597

Mean of portfolio returns sorted on ret_12_1

ret_12_1_class

H 0.012

2 0.008

3 0.007

4 0.006

L 0.005

H-L 0.007

Name: futret, dtype: float64

ret_12_1_class

H 5.836

2 4.989

3 3.864

4 3.393

L 2.006

H-L 4.215

Name: futret, dtype: float64

mean t-val

ret_12_1_class

H 0.012 5.836

2 0.008 4.989

3 0.007 3.864

4 0.006 3.393

L 0.005 2.006

H-L 0.007 4.215

2-D sort

# Let's make a 5x5 portfolios on char and char2.

char2 = 'me'

char_class2 = char2 + '_class'

split2 = 5

labels2 = ['S', 2, 3, 4, 'B', 'S-B']

# Classify stocks based on char2 in ascending order.

data[char_class2] = classify(data[char2], split2, ascending=True)

# Make 5x5 portfolios.

# qpfs2 will have index = date/char_class/char_class2 and columns = ['futret'].

qpfs2 = two_dim_sort(data, char_class, char_class2, ret_col, weight_col=weight_col)

# Make char_class2 as columns. Now columns are ['S', 2, 3, 4, 'B', 'S-B']

qpfs2 = qpfs2.unstack()

qpfs2.columns = qpfs2.columns.droplevel(0)

# Name the portfolios. We relabel after unstacking as `unstack()` sort values.

relabel_class(qpfs2, labels)

relabel_class(qpfs2, labels2, axis=1)

# Calculate the time-series mean and t-value of the future return for each portfolio.

avg, tval = time_series_average(qpfs2, cov_type='HAC', cov_kwds={'maxlags': 12})

print(f'\n Mean of portfolio returns sorted on {char} and {char2}')

print(avg)

print(tval)

Output:

Mean of portfolio returns sorted on ret_12_1 and me

me_class S 2 3 4 B S-B

ret_12_1_class

H 0.035 0.016 0.014 0.013 0.010 0.025

2 0.027 0.011 0.010 0.010 0.008 0.019

3 0.025 0.010 0.009 0.008 0.006 0.019

4 0.024 0.009 0.007 0.007 0.006 0.018

L 0.030 0.006 0.005 0.005 0.003 0.027

H-L 0.005 0.010 0.009 0.008 0.007 -0.002

me_class S 2 3 4 B S-B

ret_12_1_class

H 11.994 6.911 6.089 5.887 5.109 10.926

2 9.127 5.415 4.613 5.342 4.725 8.555

3 9.143 4.843 4.072 4.148 3.585 9.163

4 8.261 3.857 3.242 3.303 3.322 9.258

L 8.391 2.211 1.796 1.974 1.405 10.429

H-L 2.293 5.520 5.356 4.905 4.077 -1.411

Firm-level cross-sectional regression

Regress return cross-sectionally on the t-1 characteristic and other variables at each date t. Take the time-series average of the coefficients and examine their significance.

# X: For simplicity, we will only use the characteristic and the size.

exog_cols = [char, 'me']

# Run the regressions. This function returns the average coefficients, t-values, and coefficients time-series.

avg, tval, coef = crosssectional_regression(data, ret_col, exog_cols, add_constant=True, cov_type='HAC',

cov_kwds={'maxlags': 12})

print('\nMean of the coefficients')

print(pd.concat([avg, tval], axis=1))

print('\nCoefficients time-series')

print(coef)

Output:

Mean of the coefficients

mean t-stat

const 0.012 5.838

ret_12_1 0.007 4.177

me -0.000 -2.450

Coefficients time-series

const ret_12_1 me

1927-01-31 0.015 0.005 -0.000

1927-02-28 0.064 -0.018 -0.000

1927-03-31 -0.025 0.046 0.000

1927-04-30 -0.012 0.050 0.000

... ... ...

2020-09-30 -0.031 0.012 -0.000

2020-10-31 0.028 -0.013 -0.000

2020-11-30 0.194 0.008 -0.000

2020-12-31 0.087 -0.013 -0.000

Factor regression

Regress quantile portfolios’ returns on the FF-3 factors.

# Sample period.

sdate = '1952-01'

edate = '2020-12'

qpfs = qpfs[sdate:edate]

# Read factors.

# Here I use the factors generated by PyAnomaly. You can use different sources if you like.

factors = read_from_file(config.factors_monthly_fname)

# factors = WRDS.read_data('factors_monthly') # factors from K.French website.

# X: Constant + FF3.

X = factors.loc[sdate:edate, ['mktrf', 'smb_ff', 'hml']].values

# X = factors.loc[sdate:edate, ['mktrf', 'smb', 'hml']].values # If you use K. French data.

X = sm.add_constant(X)

# Run the regression for each portfolio.

result = {}

for pf in qpfs.index.get_level_values(-1):

# y: Returns of a portfolio

y = qpfs.loc[(slice(None), pf), 'futret'].values

model = sm.OLS(y, X).fit()

# Make an output table.

result[pf] = pd.DataFrame({'coefs': model.params, 'tval': model.tvalues}, index=['const', 'mktrf', 'smb', 'hml'])

result = pd.concat(result, axis=1)

print('\nFactor regression: FF3')

print(result)

Output:

Factor regression: FF3

H 2 3 4 L H-L

coefs tval coefs tval coefs tval coefs tval coefs tval coefs tval

const 0.005 7.125 0.002 3.685 0.000 0.925 -0.001 -2.154 -0.005 -5.758 0.011 7.424

mktrf 1.028 56.623 0.964 79.587 0.951 87.918 1.004 77.950 1.223 56.655 -0.195 -5.705

smb 0.201 7.141 -0.111 -5.907 -0.093 -5.537 -0.028 -1.423 0.258 7.718 -0.057 -1.082

hml -0.479 -22.131 -0.097 -6.720 0.100 7.717 0.312 20.317 0.587 22.812 -1.066 -26.172

Example 6

Quantile portfolio construction and performance evaluation.

This example demonstrates how to construct quantile portfolios (and the long-short) based on a firm characteristic and evaluate their performance.

Tercile portfolios will be generated from the 12-month momentum.

Different ways of setting the transaction cost will shown.

It is assumed that the firm characteristic has been created and saved to ‘crspm.pickle’.

Set variables

char = 'ret_12_1' # 12-month momentum

char_class = char + '_class' # Group column: portfolio-stock mapping

ret_col = 'futret' # Future return column

weight_col = 'me' # Market equity column

split = 3 # Tercile. You can also do split = [0.2, 0.8] for 2:6:2 split.

labels = ['H', 'M', 'L', 'H-L'] # Portfolio names: 'H-L' for long short.

Load data

# Read crspm data (not raw data but the output data).

data = read_from_file('crspm')

# NYSE me

data['nyse_me'] = np.where(data.exchcd == 1, data[weight_col], np.nan)

# Make the future return. If it's already in the data, this step can be skipped.

data[ret_col] = make_future_return(data['ret'])

# Let's just keep the data we need. Below is the same as `data = data[[char, ret_col, weight_col]]`

# but faster and more memroy efficient.

keep_columns(data, [char, ret_col, weight_col])

# Risk-free rates.

# Don't forget to set `month_end=True` since the crspm date has also been shifted to month end.

rf = WRDS.get_risk_free_rate(month_end=True)

Transaction costs

PyAnomaly provides a powerful way to set transaction costs via TransactionCost class.

See pyanomaly.tcost module for details.

Below are some examples of setting transaction costs.

# No transaction costs.

costfcn = None

# Transaction cost of 30 basis points.

costfcn = 0.003

# 20 (30) bps when buying (selling).

costfcn = TransactionCost(buy_linear=0.002, sell_linear=0.002)

In this example, we will assume transaction cost that decreases over time and with size.

costfcn = TimeVaryingCost(data[weight_col])

Portfolio construction

In PyAnomaly, Portfolio class is used to make a portfolio from position information.

The make_position() function converts a panel data to position data that is used as the input to Portfolio class.

In the panel data, the future return at t is the return between t and t+1, whereas in the position data, dates are shifted

so that the future return at t is the return between t-1 and t.

# Here, we remove small-cap stocks after setting the cost function.

# This is because `TimeVaryingCost` requires all firms' me as the input.

data = filter(data, weight_col, (0.2, None), by='nyse_me')

# Classify data on char. The highest momentum stock will be labeled 0 and the lowest 2.

data[char_class] = classify(data[char], split, ascending=False)

# Make position data.

# Set weight_col = None for equally-weighted portfolios.

# `other_cols` are the columns you want to keep in the position data.

position = make_position(data, ret_col, weight_col, char_class, other_cols=None)

# Make portfolios. `portfolios` will have four portfolios, 'H', 'M', 'L', and 'H-L'.

portfolios = make_quantile_portfolios(position, char_class, rf=rf, costfcn=costfcn, labels=labels)

Performance evaluation

Portfolios can be evaluated using Portfolio.eval() for a single portfolio or Portfolios.eval() for a

collection of portfolios.

# `annualize_factor=12` will annualize the results as crspm is monthly data.

pfperfs, pfvals = portfolios.eval(annualize_factor=12)

# Performance metrics.

print('\nPerformance')

print(pfperfs)

# Time-series of portfolio value, return, ...

print('\nValues')

print(pfvals)

Output:

Performance

H M L H-L

mean 0.042 -0.032 -0.029 -0.114

std 0.195 0.190 0.247 0.167

sharpe 0.215 -0.170 -0.118 -0.681

cum 5.176 -1.661 -2.466 -12.287

mdd 0.818 0.985 0.990 1.000

mdd start 1929-08-31 1929-08-31 1929-01-31 1932-06-30

mdd end 1942-04-30 1982-07-31 1982-07-31 2020-12-31

msd 0.422 0.505 0.608 0.784

msd start 1937-07-31 1932-02-29 1932-02-29 1932-06-30

msd end 1938-01-31 1932-06-30 1932-06-30 1932-09-30

turnover 5.614 7.738 6.260 12.263

lposition 456.613 458.740 458.704 456.613

sposition 0.000 0.000 0.000 458.704

Values

ret exret val1 val lposition sposition cost tover netret grossret netexret grossexret cumret drawdown drawdur drawstart succdown succdur succstart

H H H H H H H H H H H H H H H H H H H

1927-01-31 0.001 -0.002 1.001 1.000 120 0.000 0.000 0.000 0.001 0.001 -0.002 -0.002 0.001 0.000 0.000 1927-01-31 0.000 0.000 1927-01-31

1927-02-28 0.041 0.039 1.050 1.001 122 0.000 0.008 0.415 0.041 0.049 0.039 0.046 0.041 0.000 0.000 1927-02-28 0.000 0.000 1927-02-28

1927-03-31 0.010 0.007 1.073 1.050 123 0.000 0.013 0.720 0.010 0.022 0.007 0.019 0.051 0.000 0.000 1927-03-31 0.000 0.000 1927-03-31

... ... ... ... ... ... ... ... ... ... ... ... ... ... ... ... ... ... ... ...

2020-10-31 -0.028 -0.028 246929.635 253650.609 726 0.000 280.481 0.197 -0.028 -0.026 -0.028 -0.027 5.039 0.077 2.000 2020-08-31 0.077 2.000 2020-08-31

2020-11-30 0.101 0.101 272302.967 246929.635 727 0.000 310.721 0.222 0.101 0.103 0.101 0.103 5.135 0.000 0.000 2020-11-30 0.000 0.000 2020-11-30

2020-12-31 0.041 0.041 283833.135 272302.967 736 0.000 306.903 0.197 0.041 0.042 0.041 0.042 5.176 0.000 0.000 2020-12-31 0.000 0.000 2020-12-31

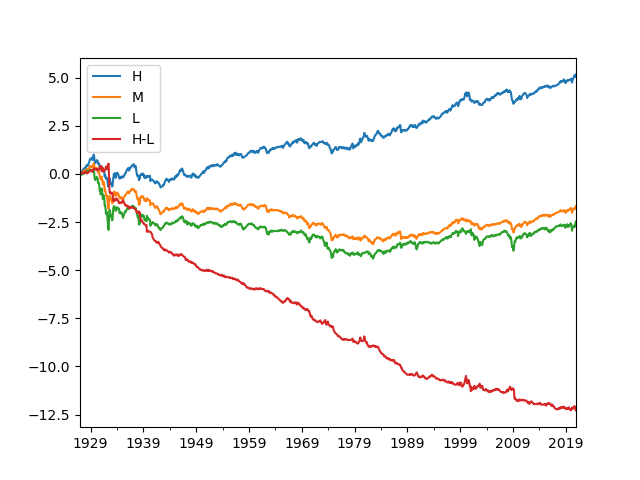

Let’s plot cumulative returns.

pfvals['cumret'].plot()

plt.show()

Output:

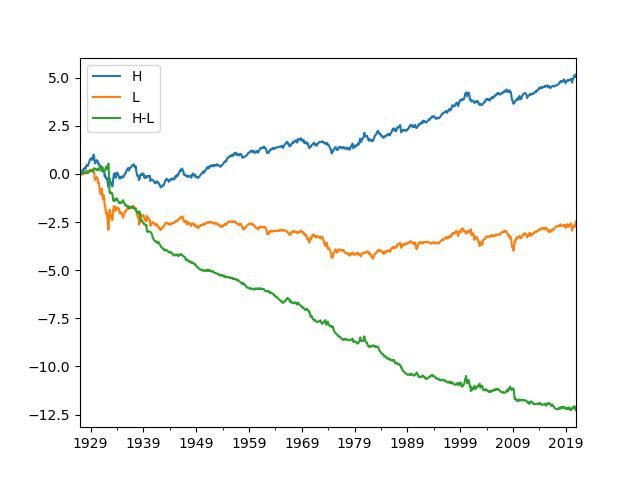

You can also plot selected portfolios.

pfvals['cumret'][['H', 'L', 'H-L']].plot()

plt.show()

Output:

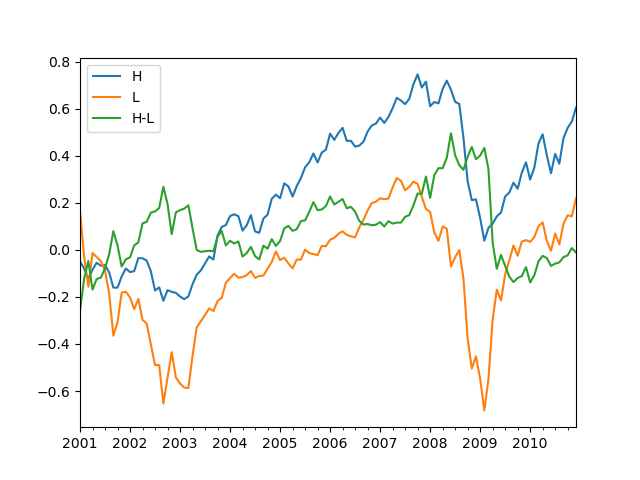

You can evaluate the portfolios for a sub-period and choose to ignore transaction costs.

pfperfs1, pfvals1 = portfolios.eval(sdate='2001-01-01', edate='2010-12-31', annualize_factor=12, consider_cost=False)

print('\nPerformance: 2001-01 - 2010-12')

print(pfperfs1)

pfvals1['cumret'][['H', 'L', 'H-L']].plot()

plt.show()

Output:

Performance: 2001-01 - 2010-12

H M L H-L

mean 0.054 0.023 0.033 0.020

std 0.169 0.149 0.256 0.201

sharpe 0.318 0.154 0.130 0.102

cum 0.605 0.330 0.219 -0.011

mdd 0.507 0.447 0.628 0.470

mdd start 2007-10-31 2007-10-31 2007-05-31 2008-06-30

mdd end 2009-02-28 2009-02-28 2009-02-28 2010-01-31

msd 0.398 0.255 0.396 0.402

msd start 2008-05-31 2008-08-31 2008-08-31 2009-02-28

msd end 2008-11-30 2008-11-30 2008-11-30 2009-05-31

turnover 6.308 7.591 6.138 12.930

lposition 669.283 673.458 672.458 669.283

sposition 0.000 0.000 0.000 672.458

You can access one of the portfolios, evaluate it, and view its position details.

# To access portfolio 'H'

pf_h = portfolios['H']

pf_h_perf, pf_h_val = pf_h.eval() # no annualize

# You can also access the returns of `eval()` as follows.

print('\nPerformance: H')

print(pf_h.performance) # pf_h_perf

print('\nValues: H')

print(pf_h.value) # pf_h_val

# To see the positions (constituents)

print('\nPositions: H')

print(pf_h.position)

Output:

Performance: H

H

mean 0.004

std 0.056

sharpe 0.062

cum 5.176

mdd 0.818

mdd start 1929-08-31

mdd end 1942-04-30

msd 0.422

msd start 1937-07-31

msd end 1938-01-31

turnover 0.468

lposition 456.613

sposition 0.000

Values: H

ret exret val1 val lposition sposition cost tover netret grossret netexret grossexret cumret drawdown drawdur drawstart succdown succdur succstart

1927-01-31 0.001 -0.002 1.001 1.000 120 0.000 0.000 0.000 0.001 0.001 -0.002 -0.002 0.001 0.000 0.000 1927-01-31 0.000 0.000 1927-01-31

1927-02-28 0.041 0.039 1.050 1.001 122 0.000 0.008 0.415 0.041 0.049 0.039 0.046 0.041 0.000 0.000 1927-02-28 0.000 0.000 1927-02-28

1927-03-31 0.010 0.007 1.073 1.050 123 0.000 0.013 0.720 0.010 0.022 0.007 0.019 0.051 0.000 0.000 1927-03-31 0.000 0.000 1927-03-31

... ... ... ... ... ... ... ... ... ... ... ... ... ... ... ... ... ... ...

2020-10-31 -0.028 -0.028 246929.635 253650.609 726 0.000 280.481 0.197 -0.028 -0.026 -0.028 -0.027 5.039 0.077 2.000 2020-08-31 0.077 2.000 2020-08-31

2020-11-30 0.101 0.101 272302.967 246929.635 727 0.000 310.721 0.222 0.101 0.103 0.101 0.103 5.135 0.000 0.000 2020-11-30 0.000 0.000 2020-11-30

2020-12-31 0.041 0.041 283833.135 272302.967 736 0.000 306.903 0.197 0.041 0.042 0.041 0.042 5.176 0.000 0.000 2020-12-31 0.000 0.000 2020-12-31

Positions: H

id ret wgt rf exret val val1 val0 cost

date

1927-01-31 10049 -0.027 0.004 0.002 -0.030 0.004 0.003 0.004 0.000

1927-01-31 10102 -0.018 0.002 0.002 -0.020 0.002 0.002 0.002 0.000

1927-01-31 10129 -0.007 0.003 0.002 -0.009 0.003 0.003 0.003 0.000

... ... ... ... ... ... ... ... ...

2020-12-31 93369 0.184 0.000 0.000 0.184 32.099 38.018 31.771 0.002

2020-12-31 93393 0.092 0.000 0.000 0.092 13.010 14.207 12.877 0.001

2020-12-31 93436 0.243 0.027 0.000 0.243 7299.521 9075.147 7225.128 0.391

Example 7

New table download.

This example demonstrates how to download a new table from WRDS. Different ways of downloading comp.secm table are demonstrated.

Connect to WRDS.

wrds = WRDS(wrds_usename)

Method 1: Download the entire table at once.

wrds.download_table('comp', 'secm', date_cols=['datadate']) # 'datadate's type will be converted to datetime.

Method 2: Download the entire table asynchronously.

This downloads data every interval years along date_col. This is a memory efficient way of downloading a large dataset.

For a small size data, this can be slower than download_table().

wrds.download_table_async('comp', 'secm', date_col='datadate', date_cols=['datadate'], interval=5)

Method 3: Download only some fields.

sql = 'datadate, gvkey, cshoq, prccm'

wrds.download_table_async('comp', 'secm', sql=sql, date_col='datadate', date_cols=['datadate'])

Method 4: Download data using a complete query statement.

Below is equivalent to the above. Note that the query statement must contain ‘WHERE [date_col] BETWEEN {} and {}’.

sql = f"""

SELECT datadate, gvkey, cshoq, prccm

FROM comp.secm

WHERE datadate between '{{}}' and '{{}}'

"""

wrds.download_table_async('comp', 'secm', sql=sql, date_cols=['datadate'])